Orbital Data Center Economics – Why AI Compute is Migrating to Orbit

Updated on June 24, 2026

Author: David Siegenthaler

This report examines the physical, operational, and financial viability of space-based high-performance computing, focusing on SpaceX’s disruptive launch and satellite manufacturing infrastructure. By evaluating the newly disclosed AI1 satellite design against traditional ground-based facilities, this analysis maps the near-term economic parity, long-term total cost of ownership advantages, and ultimate valuation of orbital data center networks.

Ultimately, we outline how scaling to a 0.5 TW off-grid planetary intelligence layer creates an unassailable infrastructure monopoly, separating the advancement of artificial intelligence from earth-scale power and grid bottlenecks.

Key messages

-

Economic Parity: Orbital Data Centers (ODCs) based on SpaceX AI1 Satellite design could become cost-competitive with Terrestrial Data Centers (TDCs) at launch costs of ~$500/ kg, depending on ultimate satellite production costs and terrestrial electricity rates.

-

Launch Cost Deflation: We project launch costs to drop to as little as $20 per kg to LEO once Starship reaches full rapid reusability stage, representing a ~100x cost decrease compared to commercial launch options available today.

-

Scale of Operations: SpaceX could reach 10,000 Starship flights per year by 2040, while annual AI compute additions could reach 100 GW, culminating in 0.5 TW of total permanent orbital AI compute deployed.

-

TCO Advantage: Total Cost of Ownership of ODCs could become ~70% cheaper than TDCs today, while scaling capacity unconstrained by land, power or grid limitations.

-

Logistical Spillover: The high launch cadence needed to sustain ODCs will democratize commercial space travel, potentially reducing individual ticket prices below $100,000 by 2040.

-

Structural Monopoly: SpaceX maintains an unassailable moat by controlling the complete end-to-end stack: heavy-lift launch capability, automated mass satellite production, and an active ground station network.

-

Vertical Integration: Additional cost savings could be realized through custom, in-house chip design and manufacturing as proposed via the Terafab project, further cementing the physical AI infrastructure dominance.

-

Preliminary Valuation: We value the SpaceX ODC business opportunity at around USD 1.3 trillion, driven primarily by the rate of Starship development and launch cadence scaling.

-

Planetary Intelligence: We believe the terminal objective is an off-grid computing layer powering millions of distributed kinetic edge agents such as the Tesla Cybercab autonomous vehicles and Optimus humanoid robots.

Note: This analysis represents our current best estimate based on publicly available information as of the date of this report. This outlook may change materially as new information becomes available. Please refer to our Legal Disclaimer for additional details.

Part 1: A Ground-Up Cost Model and Break-Even Analysis for Terrestrial vs. Space-Based (Orbital) AI Data Centers

The global compute landscape is currently navigating a structural transformation, shifting from centralized cloud architectures to "AI Factories" designed for massive-scale model training and real-time inference. This transition has placed an unprecedented strain on terrestrial infrastructure, where power availability and land acquisition have become the primary constraints on growth. As hyperscalers project capital expenditures to reach an unprecedented $750 billion in 2026, the industry is exploring radical alternatives to traditional ground-based infrastructure.

The most compelling alternative is the deployment of Orbital Data Centers (ODCs). While the concept of space-based solar power (SBSP) has captured the imagination of engineers for decades, it has historically been throttled by the massive efficiency losses and prohibitive capital costs associated with wireless power transmission (e.g., laser or microwave beam-down to Earth). ODCs circumvent this transmission bottleneck entirely. By consuming electricity directly where it is generated, in Low Earth Orbit (LEO), ODCs convert raw solar energy into high-value data packets, which are then transmitted to the ground via high-bandwidth optical links, unlocking a viable economic path for space-based energy.

LEO offers a solar irradiance of approximately 1.361 kW/m², which is roughly 40% higher than the peak solar irradiance filtered by the Earth's atmosphere. Furthermore, an orbital asset in a sun-synchronous orbit (SSO) experiences near-continuous solar exposure, achieving a capacity factor of 95% to 99%, compared to typical terrestrial solar capacity factors of just 15% to 25%. This continuous, high-density energy source provides the ultimate foundation for power-dense AI compute, bypassing terrestrial grid congestion entirely.

However, translating this physical advantage into commercial reality is a complex optimization problem involving satellite production, launch logistics, thermal radiation physics, and the comparative lifecycle economics of terrestrial versus space-based assets. To address this challenge, this report constructs a comprehensive, ground-up cost comparison model to identify the specific launch cost per kilogram ($/kg) at which ODCs achieve financial parity with terrestrial facilities. By deconstructing both the terrestrial megawatt (MW) and the orbital satellite node, specifically modeled on the SpaceX AI Sat Mini concept, this analysis accounts for the total cost of ownership (TCO), providing a rigorous breakdown of capital expenditures (CAPEX) and operating expenditures (OPEX).

Crucially, this report bridges the gap between theoretical economic parity and operational reality by mapping these cost thresholds directly against the deployment roadmap of SpaceX’s Starship. We evaluate whether and when Starship can realistically achieve the required $/kg cost threshold. By deconstructing the progression of rapid reusability, moving from initial booster and ship recovery to the highly optimized, high-cadence turnaround stages required to maximize payload mass to orbit, we project a deployment timeline and establish the vehicle's ultimate theoretical cost floor. Ultimately, this analysis identifies the intersection where heavy-lift launch economics transition orbital AI compute from a speculative alternative into a commercial inevitability.

1.1. Terrestrial Data Center Architecture

The standard unit of measure for TDC capacity is the megawatt (MW), a metric that encompasses the power delivery, cooling, and structural support required to maintain a specific IT load. In the current market, the definition of a "standard" facility is being redefined by the power density requirements of artificial intelligence.

1.1.1 TDC Capital Expenditures (CAPEX)

TDC construction costs are bifurcated by the complexity of the workloads they are intended to support. Traditional enterprise or colocation facilities typically range from $10 million to $12 million per MW. However, AI-optimized facilities, which require liquid cooling, higher voltage distribution, and reinforced structural elements for dense GPU racks, have seen costs escalate to over $20 million per MW, with some fully-built out hyperscale ecosystems reaching headline figures of $45 billion to $55 billion per gigawatt (GW).

The capital budget for a terrestrial facility is dominated by Mechanical, Electrical, and Plumbing (MEP) systems, which can account for up to 50% of the total expenditure. MEP, including substations, backup generators, and uninterruptible power supplies (UPS), represent the largest cost driver, ranging from $8.5 million to $11.5 million per MW. This is driven by the stringent redundancy requirements (typically N+1 or 2N) necessary to ensure five-nines reliability for continuous AI training cycles.

Land acquisition, while representing a smaller percentage of total CAPEX (typically 10% to 15%), has become a significant barrier to entry; prices in primary markets like Northern Virginia (NoVA) have exceeded $8 million per acre as developers scramble for sites with near-term power availability. This initial investment of $2.0 million to $3.0 million per MW is followed by the Shell & Core construction, which accounts for approx. 15% to 20% of total costs ($3.0M – $4.5M per MW). Unlike traditional builds, AI facilities require significant structural reinforcement to handle the increased floor loading of high-density GPU clusters and the weight of specialized cooling fluids.

Parallel to these electrical demands is a fundamental shift in Mechanical & Cooling infrastructure, which captures approx. 15% to 20% of the CAPEX. As thermal profiles exceed the capabilities of traditional air-cooling, developers are investing $4.0 million to $6.0 million per MW in liquid-to-chip technologies.

When accounting for interior fit-out and security, which adds another $1.5 million to $2.5 million per MW for high-security perimeters and IT support, the total CAPEX for an AI-optimized facility sits between $19.0 million and $27.5 million per MW. Based on the economic useful life of the various components, we estimate annualized CAPEX (depreciation costs) of $1.26 million to $2.81 million per MW.

Figure 1: Cost components of AI-Optimized TDC facilities, excl. IT Equipment/ AI Hardware (values in real 2025 USD).

Methodological Note on Scope: This baseline asset model evaluates facility-level infrastructure. It explicitly excludes active AI compute hardware (e.g., GPU/ TPU silicon and high-bandwidth networking fabrics), as procurement costs for these components are assumed to be identical for both TDCs and ODCs. Incremental capital expenses unique to space-based assets, such as radiation hardening and aerospace-grade component qualification, are addressed independently in the orbital cost modeling section of this report.

1.1.2 TDC Operational Expenditures (OPEX)

Beyond initial construction, the operational phase of an AI-optimized terrestrial facility generates a total annual OPEX ranging from $1.18 million to $2.04 million per MW. This recurring budget is overwhelmingly dominated by electricity, which accounts for 50% to 70% of total expenditures, or $0.74 million to $1.26 million per MW annually. Although modern facilities target highly efficient Power Usage Effectiveness (PUE) ratios of 1.1 to 1.3, their financial viability remains deeply tied to regional utility markets. In primary US markets, industrial electricity rates for large-scale data centers range from $0.06 to $0.10 per kWh, while high-cost regions like California can exceed $0.19 per kWh.

The remaining operational profile is driven by specialized upkeep and overhead. Infrastructure maintenance requires $0.15 million to $0.30 million per MW annually, reflecting the intensive preventive care mandated by high-capacity power distribution systems and liquid-cooling loops operating under near-constant thermal stress. Fixed overhead costs further burden the operating model, with property taxes and insurance comprising 15% to 20% of the total budget, and 24/7 technical staffing capturing the final 10% to 15%. Ultimately, because ongoing expenditures are so heavily weighted toward power, a facility's long-term commercial viability is dictated entirely by its ability to secure low-cost, reliable energy and remain insulated from grid price volatility.

Figure 2: OPEX of AI-Optimized TDC facility, excl. IT Equipment/ AI Hardware (values in real 2025 USD).

1.1.3 TDC Total Expenditures

When aggregating the annualized depreciation of the physical facility with the recurring operational expenses, the total annualized cost to power 1 MW of AI compute sits between $2.44 million and $4.85 million. This figure represents the "all-in" annual price of the underlying infrastructure to bring the GPUs/ TPUs online.

This cost benchmark is not static; it is subject to significant upward pressure. As the industry grapples with grid congestion and the "waitlist" for utility-scale substations grows, the premium for power-ready sites will likely continue to climb. Consequently, these figures could rise substantially in the coming years due to land and power constraints, potentially shifting the investment focus toward secondary markets or novel "off-grid" energy solutions to mitigate the escalating costs of primary-market development. Or toward Space/ ODC architectures as we will explore in the next section.

1.2. Orbital Data Center Architecture (AI1 satellite)

At the Terafab event on March 21, 2026, SpaceX and Tesla unveiled a vertically integrated vision for "civilizational-scale" AI infrastructure designed to offload energy-intensive training and inference workloads to LEO. This strategic pivot, corroborated by recent FCC filings and SpaceX’s S-1 filing, centers on the deployment of a massive constellation of ODCs to systematically bypass the power limitations, grid congestion, and land scarcity currently throttling terrestrial expansion.

Figure 3: AI1 Satellite physical dimensions and structural layout. (Source: SpaceX)

The foundational node of this space-based compute architecture is the AI1 satellite, as detailed in a SpaceX video on June 8, 2026 on X. To maximize solar collection while optimizing orbital aerodynamic profiles, each platform features a standardized structural footprint with a 70-meter wingspan and a deployed height of 20 meters. The platform is engineered around a centralized compute core powered by a 150 kW solar array, which delivers an efficient operational baseline of 250W/m².

Thermal management for the high-density processing core is sustained via a 110m² deployable liquid radiator array equipped with redundant pumping loops and integrated micrometeoroid shielding to maintain long-term asset reliability in volatile ionizing environments. This tightly optimized power and thermal distribution architecture delivers a 150 kW peak and continuous 120 kW average compute payload, yielding a derived specific power metric of 70 kW/ton. Crucially, the platform utilizes an interchangeable compute provider design, cleanly decoupling the structural satellite bus from the underlying silicon to allow for flexible chip usage.

1.2.1 ODC Capital Expenditures (CAPEX)

By adopting the core architectural parameters disclosed by SpaceX, this model normalizes its financial baseline against the company's verified engineering targets. The baseline architecture establishes a 150 kW peak solar generation capacity and an active 110 m² double-sided radiator array. Taking over these primary assumptions allows us to systematically derive secondary specific variables to complete our hardware framework.

First, utilizing the stated solar energy density of 250 W/m², we calculate a required deployable solar footprint of 600m² to harvest the necessary orbital flux. Second, by applying the disclosed processing density threshold of 70 kW of compute power per ton against the 150 kW peak load, the total mass of the vehicle is anchored at ~2,143 kg. From these figures, we can derive the platform's specific engineering mass margins: the vehicle yields a specific peak power ratio of 14.29 kg/kW, which shifts to 17.86 kg/kW when measured directly against the net 120 kW average AI compute power remaining after accounting for thermal, logic bus, and communication overhead.

While structural metrics are tightly bounded by these disclosures, manufacturing expenditures require strategic speculation. Elon Musk explicitly noted that the AI1 design is "easier to build" than communication-heavy Starlink predecessors. Consequently, this model assumes the AI1 satellite can be fabricated at half the production cost per kilogram of a Starlink V2 Mini-O (~$348/kg vs. ~$696/kg).

This 50% cost compression is driven by two distinct structural factors:

-

Hardware Simplification: The complete elimination of complex, high-cost phased-array antennas and reduced communications hardware radically reduces component-level CAPEX.

-

Mass Dilution via Commodity Elements: The massive 600 m² solar array utilizes relatively cheap, highly repeatable photovoltaic surfaces. Because this simpler, lower-cost system makes up a significantly larger percentage of the satellite's total mass, it structurally drags down the blended dollar-per-kilogram manufacturing profile of the entire asset.

At scale, an automated, automotive-style mass production line is projected to compress the unit bus fabrication cost to approximately $745,000 (excluding active AI silicon). This positions the AI1 as a highly optimized, capital-efficient deployment node that runs on a compressed 5-year economic useful life to deliberately match terrestrial GPU lithography obsolescence cycles.

Figure 4: Estimated specifications of the AI Sat Mini based on Starlink V2 Mini-O satellite.

1.2.2 ODC Operational Expenditures (OPEX)

While the initial capital requirements for orbital infrastructure are substantial, the long-term economic advantage of ODCs becomes apparent when analyzing the structural shift in Operating Expenditure (OPEX). Based on our comparative modeling, the total annual OPEX for an AI-optimized ODC at scale is estimated to range between $0.24 million and $0.43 million per MW, a staggering reduction compared to the $1.18 million to $2.04 million required for a TDC.

Figure 5: Operating cost structure of ODCs compared to terrestrial facilities.

The primary driver of this delta is the elimination of utility costs. In a terrestrial environment, electricity is the single largest operational burden, often exceeding $1 million per MW annually. In contrast, the ODC produces its own power in-orbit via the 600m² solar arrays previously discussed. Because the "fuel" source is constant solar irradiance, the cost of power is essentially front-loaded into the CAPEX of the satellite bus, reducing the recurring energy bill to zero. Furthermore, the physical maintenance profile of the ODC shifts from on-site mechanical repairs to remote digital management. While a TDC requires specialized crews to maintain chillers, liquid cooling loops, and backup generators, the ODC is essentially "maintenance-free" in orbit due to its 5-year expendable design. The remaining maintenance costs, projected at $0.075 million to $0.15 million per MW, are associated solely with the ground station infrastructure, which we anticipate will benefit from significant economies of scale by sharing the existing Starlink global network (although additional ground stations will likely be required).

Operational staffing and labor requirements follow a similar downward trend. Terrestrial facilities require 24/7 on-site technical and security personnel for each physical location. We estimate that an ODC network can be centrally managed by a leaner technical team, reducing labor costs to roughly $0.05 million to $0.10 million per MW. This centralized model leverages automated flight-control software and AI-driven network optimization, allowing a small group of engineers to oversee a vast constellation of compute nodes. This transition from "on-site" to "network-scale" management represents a fundamental decoupling of compute capacity from labor intensity.

From a regulatory and financial perspective, the ODC model avoids several terrestrial friction points. Because these assets reside in low-Earth orbit, they are not subject to traditional property taxes, which account for a significant portion of TDC overhead. While insurance remains a necessary cost, we project it will stabilize at roughly $0.075 million to $0.10 million per MW as launch reliability continues to improve and the volume of satellites in production drives down the "per-unit" risk (SpeceX typically does not insure its satellites). When accounting for network bandwidth (ground station backhaul) and cybersecurity, costs we estimate will remain consistent with terrestrial standards, the cumulative OPEX profile underscores a compelling economic narrative: while the ODC is (currently) expensive to launch into orbit, it is dramatically cheaper to operate. This suggests that for large-scale AI training, where energy and permitting are the primary limiters of growth, the orbital model offers a sustainable path toward lower "all-in" compute costs.

1.3. TDC vs ODC Total Expenditures

When comparing the overall economic framework of terrestrial versus orbital infrastructure, the TCO reveals a profound divergence in capital intensity. As illustrated in Figure 6 below, the total annual cost to sustain 1 MW of AI compute for a TDC stands at $3.3 million, whereas the ODC presents a significantly lower annualized profile of just $1.3 million per MW.

Electricity costs are effectively eliminated in orbit via in-situ solar generation, but the structural decoupling of the capital expenditure profiles represents an equally critical shift in asset economics.

A common misconception is that the shorter operational lifespan of space hardware closes the annualized cost gap with terrestrial facilities. In reality, the annualized CAPEX for the ODC is nearly 50% lower than its terrestrial counterpart ($1.0 million per MW for ODCs vs. $1.9 million for TDCs).

This major capital efficiency is driven by the structural realities of the two deployment models:

-

TDCs are heavily penalized by land acquisition premiums, massive civil engineering overhead, and the construction reinforced concrete facilities. While these shell-and-core assets are typically depreciated over an extended timeline to smooth out upfront costs, the absolute capital footprint remains high.

-

The ODC completely eliminates real estate overhead, heavy industrial building construction, and physical facility security. The AI1 satellite operates on a compressed 5-year economic useful life to deliberately match rapid terrestrial GPU lithography obsolescence cycles. Yet, despite this high-velocity depreciation schedule, the sheer structural simplicity of mass-produced aerospace hardware keeps the annualized CAPEX floor significantly below that of a permanent ground facility.

The commercial viability of the orbital model hinges on a fundamental break-even calculation: whether the cost of launch per megawatt is lower than the aggregate operational and capital savings achieved by the orbital facility over its five-year lifecycle.

Figure 6: TDC vs ODC annualized cost per MW comparison (excl. launch costs).

1.2.2 ODC Operational Expenditures (OPEX)

While the initial capital requirements for orbital infrastructure are substantial, the long-term economic advantage of ODCs becomes apparent when analyzing the structural shift in Operating Expenditure (OPEX). Based on our comparative modeling, the total annual OPEX for an AI-optimized ODC at scale is estimated to range between $0.24 million and $0.43 million per MW, a staggering reduction compared to the $1.18 million to $2.04 million required for a TDC.

A TDC incurs roughly $2.0 million more in annual operational and energy costs per megawatt compared to an ODC. Over a five-year hardware cycle, this represents a $10 million per megawatt "savings buffer" that can be allocated toward launch and orbital deployment.

1.4. Break-even Launch Costs

The commercial viability of orbital AI infrastructure is ultimately a race between two rapidly descending cost curves: the cost of reaching orbit and the cost of mass-producing specialized satellite hardware. To determine the "economic permission" for an ODC, we must establish the break-even launch cost, the price per kilogram at which the TCO for an ODC matches that of a TDC.

The target for orbital infrastructure is a moving one, dictated by the regional electricity rates of ground-based competitors. As shown below, the "low-cost" terrestrial barrier is becoming increasingly difficult for developers to access due to physical and regulatory constraints.

Figure 7: Regional Power Cost Profiles and Operational Constraints.

The following table illustrates the maximum allowable launch cost (USD per kg) required for an ODC to remain cost-competitive against various terrestrial electricity rates and satellite production costs.

Figure 8: Break-even launch cost threshold under varying operational parameters.

Our economic modeling reveals that the ODC's competitiveness is hypersensitive to both AI satellite manufacturing costs and the local cost of power on Earth. For instance, if an AI1 satellite can be produced for $0.37 million (representing a 75% cost reduction per kg vs V2 Mini) and can compete against a terrestrial market at 10.0 ct per kWh, the break-even launch cost is a relatively generous $750.4 per kg. However, as the terrestrial electricity price drops or satellite production costs rise, the window for orbital compute narrows. If production costs scale to $1.12 million, the maximum allowable launch cost drops to $354.3 per kg to remain competitive against cheap 6.0 ct per kWh energy. Even at the highest un-optimized baseline of $1.49 million per unit (the legacy V2 Mini cost baseline) competing against an aggressive 6.0 ct per kWh terrestrial rate, the model still yields a viable break-even threshold of $215.2 per kg, illustrating the robust underlying efficiency of the new design.

When we analyze these figures against current capabilities, it becomes clear that the orbital model is not yet feasible with current rocket technology. With Falcon 9 internal launch costs hovering around $1,400 per kg, even the most optimized ODC configuration cannot currently compete with terrestrial facilities. This reinforces the necessity of the fully reusable Starship platform, which is specifically designed to shatter launch costs and launch larger satellites.

Furthermore, the data highlights clear operational thresholds for manufacturing cost deflation: to achieve viability at a more near-term, intermediate launch cost target of around $500 to $600 per kg, satellite production costs must be constrained to the $0.75 million threshold (a 50% cost reduction vs V2 Mini) or lower. To become a true "TDC-alternative" capable of challenging low-cost terrestrial facilities without optimizing satellite fabrication, launch costs must comprehensively drop below $300 per kg.

Nevertheless, while absolute cost parity might remain elusive in the near term, ODCs offer a critical advantage in agility. They are significantly easier and quicker to scale than ground-based facilities, which are increasingly throttled by terrestrial power shortages, complex permitting hurdles, and increasingly negative public sentiment due to power and water usage. In this environment, a more expensive orbital build-out may still be strategically superior if it enables an accelerated compute expansion to meet unrelenting AI demand.

1.5. Key Technical Hurdles and Engineering Factors

To ensure a comprehensive analysis, a ground-up economic model must account for the steep engineering challenges inherent in operating high-density compute infrastructure in space. While this report operates on the assumption that a vertically integrated operator like SpaceX possesses the specialized aerospace experience, garnered from mass Starlink manufacturing and deployment, to successfully resolve these challenges, they remain critical variables. Each technical constraint imposes a distinct physical penalty that alters unit mass, manufacturing complexity, and asset utilization, directly shifting the baseline financial break-even thresholds.

1.5.1 Vacuum Thermal Dissipation and Radiative Scaling

The most immediate physical hurdle for an ODC is the complete absence of an atmospheric medium for convective or conductive heat transfer. Unlike terrestrial facilities that leverage ambient air or open/ closed-loop water systems to reject low-grade heat, an orbital asset must rely exclusively on passive radiative cooling to emit waste energy into the vacuum. This thermodynamic constraint is strictly governed by the Stefan-Boltzmann law, where the total power radiated (P) is proportional to the fourth power of the absolute temperature (T):

To establish a baseline for the AI1 satellite, the core compute payload is modeled with an elevated native chip junction temperature of 90°C (363.15 K, future optimized chip designs may allow for higher chip operating temperatures). Under mathematically idealized conditions, dissipating the 150 kW peak thermal waste at this temperature through a radiator array with a high emissivity (ε = 0.85) would require approximately 178.9 square meters of active radiating surface area. When translated into flight hardware, the geometric configuration directly dictates the mass penalty on the launch manifest. By configuring the thermal subsystem as a double-sided deployable fin that rejects heat from both faces simultaneously, the required physical panel footprint is cut in half, maximizing structural efficiency and keeping the baseline subsystem mass within strict launch parameters.

However, an economic and technical model must account for the physical reality of the thermal resistance penalty. Because heat only flows down a negative temperature gradient, a distinct temperature drop (∆T) is mandatory to transfer thermal energy from the 90°C silicon into the circulating coolant fluid, and subsequently from the fluid into the radiator face sheets. While TDCs operate with wide temperature buffers where coolants are 25°C to 40°C lower than the silicon to maximize ground-based chilling efficiency, an orbital asset cannot afford this luxury. The fluid loop must be kept as close to the chip temperature as possible because a hotter radiator runs exponentially more efficiently. By maximizing internal coolant fluid velocities to maintain highly turbulent flow and utilizing high-conductivity phase-change paths within the panel fabric, we speculate that the architecture can compress this thermal gradient to a tight 15°C buffer. This resistance drop implies that when the chips are running at 90°C, the actual operating temperature of the radiating surface will sit at approximately 75°C (348.15 K).

Crucially, we project that this active mechanically pumped fluid network is completely isolated to the high-density AI processors. The satellite's core bus and auxiliary subsystems, including the high-draw power distribution units, Argon-fed propulsion thrusters, and the dual-tier communication fabric, are expected to dissipate their minor thermal footprints entirely through passive chassis radiation and high-emissivity aerospace coatings, directly leveraging SpaceX’s extensive flight-proven Starlink V2 hardware heritage. Separating these thermal paths drastically simplifies fluid manifold routing and ensures that auxiliary operational heat loads never back-flow into the primary processing core.

Evaluating these parameters against the physical dimensions of the AI1 satellite confirms that SpaceX’s design is fundamentally sound and mathematically viable. Based on the official specifications disclosed on X, the vehicle deploys a 110 square meter physical radiator panel, which generates a targeted heat rejection density of 1,400 watts per square meter of physical panel footprint.

First-principles Stefan-Boltzmann calculations validate this metric with remarkable precision. Because the deployable fin is double-sided, it exposes two active faces to deep space, translating the 1,400 W/m² panel footprint into an individual face requirement of approximately 700 W/m². Substituting our derived 75°C (348.15 K) surface temperature and a standard high-emissivity aerospace coating baseline (ε = 0.85) into the formula confirms this threshold:

Multiplying this output by both active faces yields a total continuous capacity of 1,416.3 W/m² per physical square meter of footprint. This thermodynamic value slightly exceeds SpaceX's 1,400 W/m² design indication. Consequently, the 110 m² physical panel generates a total continuous heat rejection capacity of 155.8 kW (110m2 x 1,416.3 W/m2). Because the active fluid loop is dedicated exclusively to the AI accelerators, this dissipation envelope is entirely sufficient to steady the peak 150 kW compute payload while maintaining a stable, reliable safety margin for localized thermal transients.

Relying on a distributed liquid coolant network to achieve these tight temperature gradients introduces distinct capital and structural uncertainties onto the deployment manifest. Circulating pressurized fluid through a massive 110 square meter deployable panel requires a complex network of flexible fluid joints, manifolds, and headers that must fold neatly within a launch fairing and deploy flawlessly in orbit. Because liquid-filled lines add significant dead weight and introduce catastrophic single-point failure modes from potential micrometeoroid punctures, any requirement for heavy armored shielding or redundant plumbing loops will negatively impact the satellite's dry mass margins. In our economic model, this thermal resistance and structural reality translates into a strict mass contingency. If unexpected structural weight accumulates to protect the fluid loops, the economic break-even launch cost threshold drops instantly because fewer compute nodes can be manifested per heavy-lift launch, inflating the capitalized launch amortization per megawatt.

This direct-radiation model is further complicated by external environmental heat fluxes unique to LEO, which prevent the passive radiators from experiencing a perfect absolute-zero thermal sink. A satellite in SSO faces a continuous barrage of planetary albedo, solar radiation reflected off the Earth's atmosphere and cloud cover, which peaks at roughly 30% of the solar constant, or up to 400 watts per square meter. Concurrently, the planet emits outgoing longwave radiation, forcing an average of 230 to 240 watts per square meter of diffuse infrared thermal energy onto the spacecraft. This parasitic environmental flux strikes the radiator surfaces, artificially elevating the baseline temperature of the fluid loop and reducing net heat rejection efficiency. To maintain baseline performance and shield the cooling loops from this planetary thermal loading, the constellation must employ precise, dynamic attitude steering to keep the edge-on profiles of the radiator fins pointed strictly perpendicular to both the Earth's nadir and the solar vector.

1.5.2 Free-Space Optical Mesh and Network Fabric Scaling

Sustaining synchronous, massive-scale LLM training algorithms requires extreme interconnect bandwidth and ultra-low latency to manage continuous gradient and weight updates across discrete nodes. While terrestrial clusters rely on copper- or fiber-based InfiniBand and high-speed Ethernet fabrics, an orbital array must establish an identical high-performance network fabric through the vacuum of space. Standard commercial optical inter-satellite links (OISLs) optimized for third-party satellite integrations, including the standalone "Mini Laser" terminals SpaceX offers externally, typically scale to a continuous bandwidth of 25 Gbps. However, a distributed ODC fabric demands a massive operational leap, requiring a minimum throughput of 1 Tbps per node to successfully avoid localized computing bottlenecks.

SpaceX’s internal hardware ecosystem provides a critical technological foundation to bridge this performance deficit. Public engineering disclosures and official specifications confirm that native Starlink installations utilize a highly sophisticated, flight-proven optical mesh where individual laser transceivers routinely sustain throughput rates between 100 Gbps and 200 Gbps per link, routing tens of petabytes of data daily through LEO. While leveraging this proprietary heritage significantly reduces baseline development risk, scaling an AI Sat Mini constellation from a 200 Gbps communications routing mesh into a synchronized multi-terabit compute fabric remains a core engineering challenge.

Failing to clear this networking hurdle introduces severe GPU starvation, where expensive on-orbit processors sit idle waiting for data packets, crippling the financial yield of the asset. This specific architectural bottleneck is a primary focus of Google’s Project Suncatcher framework (Towards a future space-based, highly scalable AI infrastructure system design, arXiv:2511.19468), which models formation-flying clusters of solar-powered TPU nodes interconnected via free-space optical meshes operating at or above 1 Tbps. By establishing high-capacity intra-constellation optical routing, the system can execute complex model and pipeline parallelism natively in orbit, completely bypassing the throughput constraints of traditional ground-to-satellite relays.

1.5.3 Radiation Hardening, Volatile Ionizing Environments, and Component Reliability

The low Earth orbit environment subjects unshielded CMOS semiconductors to continuous cosmic radiation and solar particle events, inducing destructive Total Ionizing Dose (TID) degradation and volatile Single Event Effects (SEE), such as bit-flip errors or latch-ups. In a terrestrial facility, component degradation represents a minor operational friction handled by on-site technicians swapping server blades in minutes. In space, where physical maintenance is fundamentally impossible, system reliability must be fully capitalized upfront through structural shielding, circuit redundancy, and fault-tolerant architectures.

This harsh reality forces a critical optimization choice between utilizing low-cost Commercial Off-The-Shelf (COTS) or slightly modified terrestrial components versus investing heavily in proprietary, fully radiation-hardened space-grade silicon architectures like SpaceX's proprietary D3 platform. If ensuring a stable 5-year operational lifecycle requires heavy, traditional radiation shielding and extensive physical circuit redundancy, it will impose a significant mass penalty and a massive spike in unit manufacturing costs, causing the economic break-even launch cost threshold to drop sharply to less favorable levels.

Empirical support for a lean, COTS-centric approach has been established by Google’s Project Suncatcher framework (Towards a future space-based, highly scalable AI infrastructure system design, arXiv:2511.19468). Google’s research team conducted radiation testing on their standard TDC accelerators (Trillium TPU v6e) to simulate the LEO environment. The findings revealed that these terrestrial processors could withstand a Total Ionizing Dose (TID) of up to 15 krad(Si) without experiencing permanent hard failures, substantially higher than the shielded ~750 rad(Si) dose expected over a standard 5-year LEO mission lifecycle. While the high-bandwidth memory (HBM) arrays proved to be the most sensitive sub-components, they only began demonstrating minor performance irregularities after a cumulative dose of 2 krad(Si), which still provides a comfortable 3x safety margin over the projected baseline exposure.

This empirical benchmark strongly indicates that a 5-year orbital useful life can be achieved without relying on legacy, multi-million dollar radiation-hardened components. Instead, operators can utilize highly optimized terrestrial silicon architectures backed by software-level error correction, structural chassis shielding, and redundant node configurations. This validation preserves the mass-efficient, low-cost paradigm required to keep space-based compute competitive.

Part 2: Starship Rapidly Reusable Rocket & Launch Cost Evolution

In the preceding part, we established an economic baseline for ODCs, demonstrating that for space-based compute to achieve structural cost parity with TDCs, launch costs must compress to a threshold of approximately $500 per kg. In this section, we evaluate if and when this cost reduction is structurally achievable by analyzing the operational mechanics and scaling timelines of the first fully reusable heavy-lift launch architecture (Starship).

Historically, the trajectory of space exploration has been consistently throttled by the prohibitive cost of hardware expendability. For decades, the aerospace industry operated under a legacy paradigm where some of the most complex and expensive machines ever built were discarded after a single flight. While the Falcon 9 demonstrated the technical and financial viability of partial reusability by routinely recovering its first-stage booster, successfully lowering launch costs to a range of $1,400 to $3,300 per kg to LEO, the upper stage remained entirely expendable, leaving a high marginal cost floor.

The emergence of the SpaceX Starship represents a fundamental divergence from this paradigm, shifting the core economic focus from capital asset manufacturing to high-frequency operational logistics. The ultimate objective of this breakdown is to determine how a vehicle architecture with total development costs exceeding $15 billion can theoretically compress its marginal costs down to an unprecedented $4 million to $10 million per launch.

The following subsections dissect the specific material, propulsion, and operational levers that dictate Starship's long-term unit economics and high-frequency turnaround capacity.

2.1.1 Structural Economics and the move to Stainless Steel

The decision to utilize 304L stainless steel for the primary structure of Starship and its Super Heavy booster is the foundational driver of its long-term cost profile. Traditional aerospace structures rely on expensive carbon fiber or aluminum-lithium alloys, which are not only costly to procure but require complex processes and labor-intensive layups. Stainless steel, by contrast, is a commodity material used extensively in the maritime and industrial sectors. The manufacturing process involves unrolling rolls of stainless steel that are approximately 3.97 mm thick and welding them into rings of 9 meters in diameter. Each ring possesses a mass of approximately 1,600 kg and a height of 1.83 meters.

The cost implications of this material choice are twofold. First, the raw material cost is nearly 50 to 100 times cheaper than carbon fiber per kilogram. Second, the thermal properties of stainless steel allow the vehicle to survive atmospheric re-entry with a significantly lighter and less complex thermal protection system (TPS) than would be required for an aluminum-based airframe.

2.1.2 Propulsion Economics: The Raptor Production Line

If the airframe is the skeleton of the economic model, the Raptor engine is its heart. Propulsion is traditionally the most expensive segment of any launch vehicle. For example, the RS-25 engines used on the Space Launch System (SLS) cost approximately $100 million each. A Starship stack requires 39 engines (33 on the booster and 6 on the ship, 3 of which are vacuum-optimized). At the start of the program, Raptor 2 engines were estimated to cost between $1 million and $2 million each, meaning the engine hardware alone for a single stack represented an investment of $39 million to $78 million.

The Raptor engine utilizes a full-flow staged combustion cycle, an extremely efficient and complex architecture specifically designed to facilitate many reuses. This design necessitated a fundamental shift away from the RP-1 (refined kerosene) used in the Falcon 9’s Merlin engines. While RP-1 is a reliable, energy-dense fuel, it is prone to "coking", the buildup of solid carbon deposits that occurs when the fuel is heated in the absence of enough oxygen. In a full-flow cycle, where a fuel-/ oxygen-rich gas must drive high-speed turbine blades, this soot and coke buildup would cause rapid mechanical degradation and require extensive cleaning between flights. Liquid Methane (CH4), by contrast, burns exceptionally clean and has a much higher coking point, virtually eliminating soot accumulation and enabling the rapid, maintenance-free turnaround essential for Starship's economics. Additionally, methane offers a higher specific impulse and allows for In-Situ Resource Utilization (ISRU), as it can be synthesized on the Martian surface.

Raptor 3 takes this evolution further, featuring an integrated design that removes external plumbing and sensors while incorporating an integrated heatshield, which significantly reduces weight and manufacturing complexity. Generally, all components are designed for maximum rapid reusability to minimize turnaround time and maintenance costs between flights. SpaceX is reportedly targeting a production rate of 4,000 Raptor engines per year, which is projected to drive the cost per engine down to the $250,000 to $500,000 range.

2.1.3 Marginal Cost Analysis: Propellant and Cryogenic Fluids

In an expendable rocket, fuel accounts for a negligible percentage of the total launch price. In a fully reusable system, propellant becomes one of the largest marginal expenses. Starship uses sub-cooled liquid oxygen (LOX) and liquid methane (LCH4). Methane was chosen over hydrogen because of its higher density, which allows for smaller tanks, and its easier storage at cryogenic temperatures, which reduces the complexity of long-duration missions.

The stoichiometric mixture ratio for methane and oxygen is roughly 4:1, but the Raptor engine is optimized to run slightly fuel-/ oxygen-rich to manage heat and engine stability. Technical data suggests a mixture ratio of approximately 3.6 parts oxygen to 1 part methane.

For a Block 4 Starship stack:

Total Propellant Mass: 4,050 t (Booster) + 2,300 t (Ship) = 6,350 tonnes.

Methane Mass (LCH4): 6,350/ 4.6 = 1,380 tonnes.

Oxygen Mass (LOX): 6,350 – 1,380 = 4,970 tonnes.

Industrial oxygen is produced via air separation units (ASUs). Prices in the United States for the fourth quarter of 2025 are estimated at $250 per metric tonne. Liquid methane is derived from natural gas. The industrial price for natural gas in Texas is forecasted to average $6.32 per thousand cubic feet in early 2026. Using a conversion of roughly 18.6 kg per thousand cubic feet, the raw gas cost is approximately $340 per tonne. However, liquefaction and purification into rocket-grade methane add a premium. Industrial LNG benchmarks suggest a delivered price of approximately $400 to $500 per tonne for large industrial consumers.

Figure 9: Propellant cost breakdown and liquid methane/ oxygen mass ratios.

This calculation aligns with Musk's public estimates of $900,000 for early models, noting that the Block 4 is nearly double the size and mass of those early iterations. As SpaceX builds its own on-site ASUs and methane liquefaction plants at Starbase, the effective cost per tonne will likely drop by 20% to 30%, potentially bringing the propellant cost closer to ~$1.3 million per launch.

2.1.4 Manufacturing Cost Trajectory and Capacity Evolution

The evolution of Starship through various "Blocks" shows a consistent trend toward increased mass and capability.

Figure 10: Structural steel mass and propellant volume progression across Starship blocks. (Source: SpaceX).

The progression toward Block 4, with a propellant capacity of over 6,300 tonnes, represents a vehicle that is nearly double the mass of early prototypes. While this increases the raw material consumption, the amortized cost per kilogram of payload falls precipitously.

2.1.5 Maintenance and Refurbishment: The "Airline-Like" Goal

The economic viability of Starship hinges on the transition from traditional, labor-intensive refurbishment to a model of rapid, high-frequency turnaround. While the airframe and engines are designed for multi-flight endurance, the Thermal Protection System (TPS) remains the most critical hurdle to achieving same-day reusability.

Unlike the Space Shuttle, which utilized complex adhesive bonding, Starship (v3) is shielded by approximately 18,000 hexagonal ceramic tiles secured via a mechanical stud-and-nut system. This design is intended to allow for rapid, localized replacement. However, operational testing has revealed significant challenges during the launch phase. The extreme acoustic and vibrational environment generated by the 33 Raptor engines can shear attachment pins or cause tiles to impact one another, leading to premature shedding before the vehicle reaches orbit. Furthermore, the stainless steel hull undergoes significant cryogenic contraction when loaded with propellant; if the gap tolerances between tiles are not perfectly calibrated, this structural "shrinking" can pop tiles off their mounts.

A more profound challenge lies beneath the primary ceramic layer. SpaceX utilizes a secondary thermal barrier, a proprietary ablative material (SPAM), designed as a fail-safe. If a tile is lost or breached during re-entry, this underlying layer dissipates heat by slowly burning away.

While this prevents a catastrophic breach of the steel hull, the secondary material is fundamentally sacrificial. Once a tile is compromised and the underlying abrasive shield is "used up," a simple mechanical tile swap is no longer sufficient. These zones likely require a full overhaul and refurbishment of the secondary insulation blankets and ablative coating. This localized "patchwork" repair is significantly more complex than a standard tile replacement and threatens to ground the vehicle for extended periods.

To achieve the turnaround times necessary for Starship’s economics, with the ultimate goal of flying the vehicle multiple times per day, SpaceX will likely move away from the thousands of man-hours traditionally required for heat shield inspection.

While the Super Heavy booster is designed to return to the launch pad in as little as six to eight minutes and requires no heat shield tiles, allowing for nearly immediate restacking and reuse, the Ship presents a more complex verification challenge. To bridge this gap, the company is reportedly working toward an automated regime using drone-based high-resolution imaging and AI. These systems are designed to scan the Ship's entire surface in minutes, using computer vision to detect microscopic cracks, debonding, or ablative depletion that would be invisible to the naked eye.

The ultimate goal is an ecosystem where the Booster can be recycled almost as quickly as an aircraft, and the Ship’s Thermal Protection System (TPS) is robust enough that "refurbishment" is relegated to a minor, automated task rather than a programmatic bottleneck.

Raptor 3 is designed for a lifespan of up to 100 flights without an overhaul. In the early phase, engines are removed and inspected after every flight, adding millions to the "test flight" cost. Once the fleet achieves a high reliability threshold, engine maintenance shifts from "overhaul" to "inspection by exception." Telemetry monitors every turbopump revolution and temperature gradient. If the data is within nominal limits, the engine is cleared for the next flight without being touched. This transition from labor-intensive maintenance to data-driven operations is the cornerstone of reducing the $100 million "test" launch cost to a $4 to $10 million "commercial" launch cost.

2.2. Integrated Economic Model: From Prototype to Mature Platform

The following section explores the economic evolution of the Starship program to provide ultra-low-cost access to space. The model highlights a transition from a capital-intensive development project to a global logistics utility, where the primary cost driver shifts from hardware manufacturing to simple propellant and program overhead dilution.

Figure 11: Projected Starship Long-Term Marginal Cost Evolution and Reusability Dynamics.

2.2.1 Economic Methodology & The Three Structural Pillars

The model locks the vehicle build cost at a constant $100 million. Rather than following a traditional industrial learning curve where unit costs decline over time, the model assumes SpaceX will reinvest all production efficiencies into structural durability and volumetric scaling. The capital typically saved by manufacturing optimization is "used up" to build progressively larger, more capable airframes. This is demonstrated by the transition from Block 3 (100-tonne payload to LEO) to Block 4 (200-tonne payload to LEO). Crucially, because the SSO required for stable ODC operations are more energy-intensive than low-inclination trajectories, the model incorporates a strict 25% payload capacity penalty for all SSO calculations (reducing Block 4's operational capacity to 150 tonnes). By maintaining the $100 million production cost while doubling the baseline LEO mass capacity, the effective dollar-per-ton manufacturing asset cost is still cut in half.

To determine how this fixed capital cost drops down to competitive commercial rates, the financial model rests on three distinct economic pillars:

Pillar 1 - Capital Amortization Through Velocity: In a logistics system where depreciation dominates, a robust $100 million airframe engineered for 100 flights is vastly more lucrative than a $50 million variant that fatigues after five. The model utilizes lifetime flight counts as statistical averages to amortize this asset value. In the early reusable phase, an average hull life of 2 flights imposes a punishing $50 million depreciation charge per mission. As the platform matures to an average of 100 uses, this depreciation cost is diluted to just $1 million per flight, effectively removing the capital expense of the rocket from the launch equation.

Pillar 2 - The Lifetime Maintenance Curve: This pillar balances the divergent operational profiles and required asset ratios of the launch stack. The booster is structurally more expensive due to its 33-engine Raptor density, yet its suborbital flight path is mild. Due to the rapid turnaround of the Super Heavy booster, returning to the launch site in under ten minutes to be caught by the tower, a single booster can support multiple launches per day. In contrast, the Starship upper stage remains in orbit to deploy payloads and perform maneuvers before reentering, resulting in a much longer operational cycle. Consequently, a mature launch system requires significantly fewer Super Heavy boosters than Starships to sustain a high flight cadence. On the refurbishment front, the 6-engine ship must endure the extreme thermal cycling of Mach 25 orbital reentry, scaling the average fleet-wide refurbishment costs from an initial 8% ($8 million) down to a mature 1% ($1 million) floor. Similar to commercial jet aviation, maintenance follows a "lumpy" trajectory where cumulative life-cycle servicing will eventually exceed the initial $100 million build cost.

Pillar 3 - Fixed Overhead Dilution: Based on structural data from current financial disclosures, the Starship program carries a fixed annual overhead baseline of approximately $3 billion, covering ongoing R&D, engineering payroll, and launch complex maintenance. At low flight volumes (e.g., 10 flights per year), allocating this fixed cost adds an unsustainable $300 million burden to every single launch. When flight density scales to 10,000 launches annually, this asset overhead is spread across such a vast volume that its impact drops to an insignificant $300,000 per flight.

Beneath these three scaling pillars sits an irreducible marginal floor of ~$2 million per launch, representing the fixed commodity costs of sub-cooled liquid oxygen, liquid methane, and localized ground operations.

2.2.2 Indicative Operational Scaling Horizons

When these three pillars are combined, the model illustrates a massive cost deflation curve, compressing all-in launch costs from thousands of dollars per kilogram down to double digits over an estimated fifteen-year horizon.

The Prototype Stage (Expendable)

Current Phase

Starship operates strictly as an unrecovered R&D platform. With an annual cadence limited to test flights, the hardware is entirely sacrificed to harvest telemetry. The depreciation charge is the full $100 million build cost. Combined with un-diluted program overhead, the estimated internal all-in cost per launch is evaluated in the billions, yielding an uncommercial $20,680 per kg to SSO.

Early Commercialization (Heavy Refurbishment)

~2028

The program establishes partial reusability, scaling to roughly 10 flights annually. Airframes average 2 uses before retirement or hull loss, halving depreciation to $50 million per flight. In this early operational era, refurbishment is highly manual and labor-intensive, requiring an average budget of 8% ($8 million) per launch to handle hardware fatigue. The internal launch cost drops to $60 million (excluding overhead), yielding a marginal cost of $400 per kg to SSO, the point at which early ODC architectures begin demonstrating basic economic viability.

Achieving Full Reusability (Moderate Refurbishment)

~2031

Fleet maturity scales the launch cadence to approximately 100 flights per year. Average airframe utility climbs to 5 uses, dropping depreciation to $20 million, while refurbishment efficiencies optimize to 4% ($4 million). Crucially, the $3 billion fixed program overhead begins to dilute effectively, adding $30 million per launch. The resulting all-in cost per kilogram drops to $373 to SSO, placing space-based compute infrastructure on the absolute event horizon of cost-competitiveness with high-end TDCs.

The Rapid Reusability Breakthrough

~2035

The architecture shifts to an automated, asset-efficient "inspect-and-go" framework, pushing annual volume to 1,000 flights. Handheld inspections are replaced by automated AI drone swarms scanning for micro-defects or heat-shield debonding. Refurbishment costs collapse to 2% ($2 million). With hulls now averaging 20 uses, depreciation sinks to $5M per flight. The allocated overhead slides to a minor 0.1% ($3 million), driving the total cost per kilogram down to $80 to SSO and handing ODCs a structural cost advantage over land-based alternatives.

High Flight Density (Airline-Style Scaling)

~2040

Starship achieves a true commercial logistics profile, executing roughly 10,000 flights per year. The $3 billion annual overhead is almost completely neutralized at $300,000 per flight. Refurbishment costs hit a 1% floor ($1 million), and mature engine reliability extends airframe life to 100 uses, reducing depreciation to $1 million. The dominant cost driver shifts entirely to the $2 million marginal propellant and ground operations floor. The resulting all-in cost hits a terminal floor of $29 per kg to SSO, unlocking massive orbital computing constellations.

2.2.3 Strategic Implications: Vertical Demand and the Reusability Moat

This cost model underscores a stark reality: Starship's financial viability is hyper-dependent on industrial scale. The model suggests ~100 launches per year as the critical economic event horizon where fixed overhead dilutes enough to unlock commercial viability (for comparison, Falcon 9 completed 165 flights in 2025).

Because the open market currently lacks a natural commercial demand for hundreds of heavy-lift launches per year, SpaceX faces a severe "chicken-and-egg" problem. Low launch costs require high flight volumes to amortize fixed overhead, but those high flight volumes require a mature space economy that cannot develop while launch costs remain high.

Furthermore, translating this theoretical mathematical trajectory into an operational reality will require an extended timeline and an unprecedented volume of flights to fully master and perfect rapid reusability. Iterating through the compounding complexities of automated tower-catch logistics, localized thermal shock across thousands of ceramic tiles, and rapid multi-engine relight dynamics introduces a multi-year execution runway marked by aggressive hardware attrition. This prolonged operational stabilization phase forms an exceptionally wide technical and capital moat. Competitors cannot simply duplicate the physical stainless-steel airframe; they must replicate an empirical playbook written in real-world flight telemetry and precision automation, rendering the asset architecture profoundly difficult and cost-prohibitive to copy.

To shatter this commercial bottleneck and systematically cross this capital-intensive engineering moat, SpaceX uses a strategy of vertically integrated, captive demand, acting as its own anchor tenant. Just as Starlink provided the baseline launch volume required to optimize the Falcon 9 asset life, the ODC project serves as the economic catalyst for the Starship program. By manufacturing and launching its own compute constellations, SpaceX creates the internal flight density needed to systematically force the cost of space down to its absolute physical floor.

2.2.4 Comparative Launch Vehicle Economics (LEO Basis)

To contextualize Starship's deflationary cost curve, the compiled table isolates the global launch market across three distinct eras: legacy state-backed platforms, contemporary commercial workhorses, and future Starship operational blocks. Tracing these vectors reveals how capital hardware abandonment transitions into high-velocity asset utilization.

Methodological Note: Unlike the preceding sections of this report which evaluated performance metrics on a SSO profile, the figures presented in this comparison table are standardized strictly to a LEO trajectory. Because low-inclination LEO insertions require less delta-v (velocity change) than high-inclination polar or sun-synchronous paths, the raw payload capacities are fundamentally higher across all architectures. Consequently, this changes the baseline math, yielding a lower dollar-per-kilogram cost structure than an equivalent SSO manifest.

Figure 12: Space launch market cost comparison across current and future launch vehicles.

The data highlights a clear economic evolution from single-use hardware to high-frequency asset reuse. Legacy state-backed platforms like the Space Shuttle and Space Launch System (SLS) range from $21,000 to over $62,500 per kilogram because the vehicles are discarded after one flight. Modern commercial rockets compress retail pricing to between $1,500 and $4,300 per kilogram. This contemporary segment features a wide gap between market price and internal cost; a reusable Falcon 9 retails for ~$74 million ($3,246/kg) but costs SpaceX roughly $25 million ($1,429/kg) to launch, generating high margins to fund corporate R&D.

Starship v4 lowers this baseline using aggressive volumetric scaling. Voyager Space's SEC 10-K filing disclosed a $90 million non-cancelable launch contract to deliver the Starlab space station on Starship no earlier than 2028. Given Starship’s 200,000 kg LEO capacity, this commercial price equals $450 per kilogram, immediately matching or beating Falcon Heavy economics.

As Starship operations mature between 2030 and 2040, SpaceX's internal execution costs will fall. When refurbishment drops to a 1% floor and airframes average 100 flights, the internal cost per launch drops to a $4 million propellant and ground operations floor. This drives the final internal cost to $20 per kilogram to LEO, crushing the financial threshold required to make ODC infrastructure competitive with terrestrial facilities.

Figure 13: Cost per kg to LEO comparison; Flight Configurations: Exp = Expendable, Re = Reusable, FRe = Fully Reusable (incl. upper stage), FRRe = Fully Rapidly Reusable (without refurbishment)

Part 3: Financial Synthesis: Cost Savings, Valuation & Outlook

This section synthesizes the ODC vs TDC break-even launch costs analyzed in Part 1 with the launch logistics cost curves analyzed in Part 2.

3.1 Potential Cost Savings of ODCs vs TDCs

The table below illustrates the projected cost premium or discount (%) of an ODC deployment relative to a traditional land-based data center baseline. A positive percentage indicates a cost penalty over terrestrial alternatives, 0% represents absolute financial break-even (cost parity), and a negative percentage represents a structural cost advantage for space-based compute.

Figure 14: ODC Cost-Parity Sensitivity and Cost Saving Matrix (vs 8ct/ kWh TDCs).

The model demonstrates that long-term commercial viability hinges on two primary sensitivities: the speed of Starship development and the unit economics of mass-manufacturing the AI satellite nodes. Financial break-even could occur as early as 2028, assuming SpaceX compresses internal marginal launch costs to $400 per kg to LEO and satellite manufacturing costs drop to $1.1 million per node. Notably, this framework assumes TDC costs remain constant, establishing a conservative baseline that excludes the mounting upward cost pressures TDCs face from escalating grid constraints and power availability limitations.

Furthermore, this orbital, modular architecture unlocks a critical "Time to Power" advantage outlined in the SpaceX S-1 prospectus. While expanding terrestrial capacity typically demands building or retrofitting massive facilities, a process slowed by long lead times for power procurement, utility grid interconnections, and permitting before hardware can generate useful tokens, the space-based framework circumvents terrestrial power infrastructure constraints entirely. This baseline shift allows compute capacity to be deployed and scaled dynamically as demand grows, allowing the network to field next-generation compute hardware in quicker succession than rigid land-based facilities can manage. Notably, based on the finalized AI1 specifications, we estimate that a single Starship v4 launch can deliver 70 satellites and 10.5 MW of peak AI compute directly to SSO, highlighting the unprecedented deployment velocity of this mechanism.

By the 2040 terminal phase of the model, launch costs cease to act as the primary operational bottleneck. At an operational cadence of 10,000 launches per year, annual AI compute additions could reach 100 GW, culminating in 0.5 TW of total permanent orbital AI compute deployed. At this scale, the power consumed by the ODCs in orbit would approximately match the entire electricity consumption of the United States today. This absolute energy volume demonstrates that scaling an equivalent infrastructure layer on Earth is fundamentally unrealistic given terrestrial grid limitations and power availability constraints.

With logistics compressed to just $27 per kg to SSO, the overarching financial model is driven almost entirely by satellite asset depreciation. At a mature production cost of $0.4 million per node, a space-based infrastructure array could capture a >70% structural cost discount compared to TDCs. This terminal advantage is unlocked by eliminating land-acquisition overhead, intensive physical building infrastructure, and maximizing continuous solar energy capture in orbit.

We can quantify how much the deployment of ODCs could save in annual costs compared to contemporary TDC TCO. Because these operational cost reductions bypass traditional infrastructure overhead, every dollar saved directly translates to operating profit. At the projected mature scale of 10,000 flights per year and 0.5 TW of deployed compute, total annual cost savings would amount to approximately $1 trillion, even when evaluated at a conservative AI1 satellite production cost of $0.75 million per node.

Ultimately, substantial additional cost savings could be realized through custom, in-house chip design and manufacturing as proposed via the Terafab project. While the baseline benefits of ODCs rest on their rapid deployment speed, agility, and scaling velocity, the most profound potential for structural cost compression may lie in the full vertical integration of chip manufacturing and advanced packaging.

3.2 SpaceX’s Competitive Moat

We believe SpaceX is currently the only entity capable of translating the concept of an ODC from a theoretical model into a viable, high-margin commercial asset class. While global hyperscalers and competing aerospace firms are optimizing isolated parts of the digital or logistical stack, no other player possesses the cross-disciplinary, closed-loop infrastructure and capabilities required to realize orbital hyper-compute at scale.

Reusability is the definitive gating item for space-based business models. Without an ultra-high cadence of vehicle reflights, the upfront amortization of aerospace manufacturing and structural engineering costs completely dominates the per-flight cost structure, making space-based compute uncompetitive with ground-based alternatives.

When launch hardware is iterated to support hundreds of flights over its lifecycle, the capital allocation per launch dilutes to near-zero. This structural shift isolates the marginal operating floor to liquid propellant, ground operations overhead, and automated inspections, yielding the hyper-deflated low-Earth orbit (LEO) cost profile required to make ODCs viable.

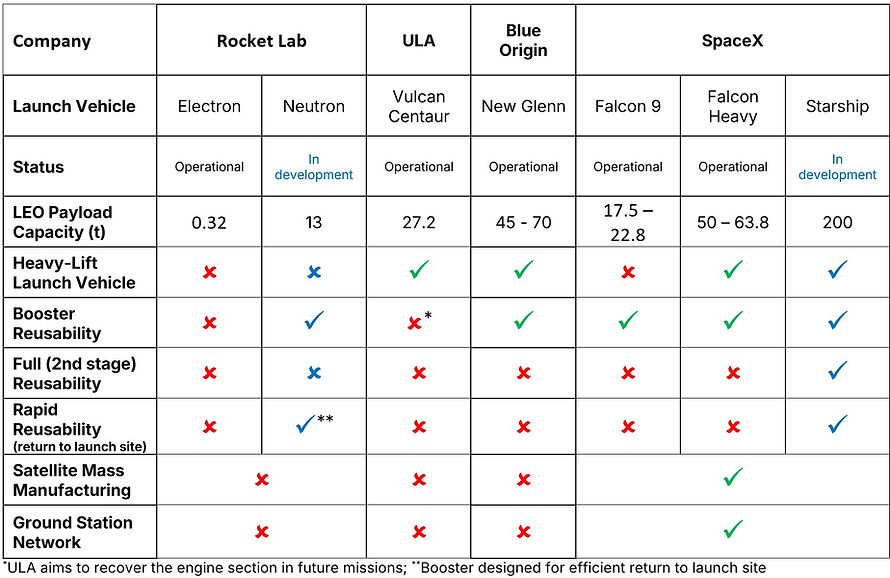

To evaluate why SpaceX holds an effective structural monopoly on this architecture, the global launch market must be analyzed across three distinct industrial capabilities: launch vehicle capabilities, satellite mass manufacturing velocity, and ground communications infrastructure.

Figure 15: Competitive Landscape Matrix of Leading Launch Providers and Space Segment Capabilities.

Mastering heavy-lift launch capabilities is entirely insufficient to build an orbital processing network. To deploy and maintain a high-density compute constellation, an operator must simultaneously master three highly complex architectural pillars:

-

Fully Reusable, High-Mass Logistics: SpaceX remains completely isolated as the only launch provider actively demonstrating and executing full, (rapid) reusability with automated mechanical tower catches. While competitors like Blue Origin, Rocket Lab, and ULA chase partial booster recovery paths (e.g., downrange barge landings, splashdowns, or engine-pod ejection), none possess a concrete development timeline or empirical telemetry path for full second-stage reusability. Because the upper stage represents a significant portion of a vehicle's manufactured value, discarding it on every mission locks competitors into a cost ceiling that kills ODC economics.

-

Automotive-Style Satellite Mass Manufacturing: Shifting server blocks to orbit requires building complex, space-hardened nodes at an unprecedented industrial scale and a rock-bottom dollar-per-kilogram cost structure. Leveraging the automated production loops engineered for Starlink, SpaceX can fabricate complex, high-power satellite buses at a massive cost discount relative to legacy aerospace providers. No other launch operator possesses a captive, vertically integrated satellite production line capable of spitting out multiple hardware nodes daily.

-

A Deeply Integrated Ground Station Network: To prevent catastrophic data starvation at the edge, processed data must be seamlessly offloaded back into the terrestrial web. SpaceX’s fully deployed Starlink ground-station network provides a low-latency communication layer that allows terabits of orbital compute to instantly integrate with land-based logistics, completely avoiding the multi-billion-dollar ground infrastructure lead times that would stall any alternative provider.

This deep structural synergy proves that SpaceX has moved far beyond its legacy classification as a commercial rocket or telecom utility. By capturing the launch platform, the automated assembly line, the global communications network, and, via the joint Terafab project, captive semiconductor design and advanced packaging, the company could soon control the complete, end-to-end compute stack.

3.3 Preliminary Valuation Framework, Scaling Dynamics, and Strategic Optionality

Within a 10- to 20-year execution horizon, our preliminary valuation model projects a mature terminal state for the space-based compute layer characterized by three core variables: an annual launch cadence of 10,000 flights, an optimized AI1 satellite production cost of $0.75 million per unit (representing a 50% cost-per-kilogram reduction relative to legacy V2 Mini architectures), and a total active orbital compute footprint of 0.5 TW. While a 0.5 TW infrastructure layer represents approximately four times the current globally installed TDC capacity, we believe long-term AI demand will comfortably absorb this capacity by 2040 through deep training workloads and real-time edge inference.

An annual run-rate of 10,000 launches translates into an operational cadence exceeding one launch per hour. While unprecedented in aerospace engineering, this cadence is structurally viable through the build-out of multi-site launch complexes utilizing multi-tower launch and catch configurations. To put this logistics layer into perspective, 10,000 annual Starship flights remains negligible compared to the global commercial aviation industry, which routinely executes over 100,000 flights per day.

Transitioning rocket logistics to an airline-style operational model is entirely dependent on Starship achieving a state of full, rapid reusability where vehicles operate back-to-back flights without manual refurbishment. This scaling trajectory is fundamentally supported by SpaceX's historical cadence curves: the company expanded its annual launch volume from just 2 flights in 2012 to 165 orbital flights in 2025. Replicating a comparable multi-year exponential growth curve would successfully scale current operations to the targeted terminal ceiling.

Applying a 25% discount rate (real as we are not applying any inflation factors in our projections) and a terminal price-to-earnings (P/E) multiple of 30x against these operational cash flows yields a baseline indicative valuation of USD 1.3 trillion for the SpaceX ODC business opportunity. However, significant timeline and execution uncertainties persist, dictated primarily by the development and qualification velocity of the Starship platform.

Figure 16: SpaceX ODC Business Opportunity Valuation Sensitivity table based on 10k flights per year, 0.75m AI1 Satellite production costs and 0.5 TW AI compute deployed.

While foundational technical capabilities have been successfully flight-proven, including automated satellite deployment mechanisms, first-stage Super Heavy booster recovery, and propulsive upper-stage ocean landings, several critical engineering milestones remain unverified. Most notably, a propulsive ship-level tower catch has yet to be executed, and the exact degree of localized structural damage and thermal engine fatigue incurred per flight remains a proprietary unknown.

Conversely, the satellite manufacturing layer carries a comparatively lower risk profile given the company's unparalleled heritage in high-cadence assembly derived from the Starlink constellation. The selection of a 20% discount rate balances these immense, unprecedented technical hurdles against an unassailable competitive moat that effectively insulates the asset from near-term replication.

Should SpaceX successfully achieve this operational scale, the terminal P/E multiple of 30x may prove conservative. The ultra-low-cost access to orbit enabled by a mature Starship logistics utility will naturally unlock profound economic spillover effects, opening up entirely new space-based industries and commercial markets. Furthermore, the baseline USD 1.3 trillion valuation carries significant structural upside due to two major vectors not explicitly capitalized in the sensitivity matrix:

-

Terrestrial Bottleneck Insulation: The current model conservatively assumes constant TDC infrastructure costs. In reality, ODC asset valuation will experience upward convexity as ground-based facilities face escalating cost premiums and extended lead times driven by primary-market grid congestion, power availability caps, and local regulatory bottlenecks.

-

The Silicon Manufacturing Flywheel: Additional margin expansion can be captured through the vertical integration of custom semiconductor design and advanced packaging via the Terafab project, structurally bypassing third-party silicon premiums to drive the capital cost of the compute payload down to pure foundry manufacturing minimums.

3.4 Conclusion: From Commercial Launch Utility to Off-Grid Infrastructure Monolith

The economic modeling developed within this report demonstrates that migrating artificial intelligence infrastructure from Earth to orbit is no longer an abstract aerospace concept, but a mathematically predictable logistics function. Based on the AI1 Satellite specifications, initial structural competitiveness with TDCs occurs at a launch cost threshold of approximately $500 per kg. Once SpaceX’s Starship architecture achieves full, rapid reusability, internal launch costs are projected to slide to a terminal floor of ~$20 per kg to LEO (~$27 per kg to SSO) by 2040. This ~100x deflationary cost curve fundamentally disrupts the infrastructure layer, translating into an all-in ~70% TCO discount compared to legacy land-based facilities.

Launch economics alone, however, won't maximize the business's profitability. Further optimization potential comes from making custom chips in-house via the Terafab project, which could bring AI infrastructure costs down even further.

This massive operational scale yields profound positive externalities for the broader space economy, driving down the marginal cost of space access for all space-related industries and democratizing commercial space travel, potentially reducing individual ticket prices below $100,000 by 2040. Concurrently, it establishes an unassailable corporate moat. To challenge this ecosystem, a competitor would have to simultaneously master three highly capital-intensive, multi-disciplinary fields:

-

Fully reusable heavy-lift logistics to minimize mass-to-orbit deployment costs.

-

Automated satellite mass manufacturing at an automotive cadence.

-

A globally distributed ground station network to handle low-latency data transfers.

Ultimately, this industrial convergence marks SpaceX's transformation from a commercial launch utility into a sovereign, off-world infrastructure monolith, an "Orbital Brain" positioned 500 kilometers above the atmosphere, entirely insulated from regional power grid failures, domestic energy rationing, and localized geopolitical strife. This planetary intelligence layer could serve as the foundational architecture for the next era of mass automation, powering and coordinating millions of distributed kinetic edge agents on the ground, such as the Tesla Cybercab autonomous vehicles and Optimus humanoid robots.

Disclosure: As of the publication date, Laniakea Research and its analysts hold no long or short positions in SpaceX, nor any related financial instruments.

Legal Disclaimer

1. No Investment Advice or Solicitation